All organizations are interested in finding opportunities to reduce overhead costs and Overhead Value Analysis (OVA) is one technique which can be used to achieve this.

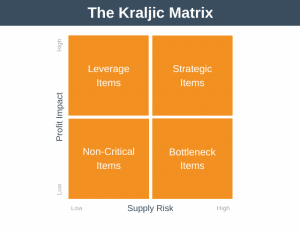

OVA focuses on a reduction in the overhead of horizontal costs (indirect costs) within an organization, such as facilities management and human resources. This is highlighted in the diagram below.

OVA can be used to eliminate excess overhead activities, but it can also be used simply to provide awareness of the demands on internal services from internal customers.

Overheads are typically made up of many thousands of small, often unrelated activities. Because these are very difficult to analyse individually, organizations have traditionally tended to issue ineffectual cost reduction edicts, such as “cut all operational costs by 15%”. Employees understandably dislike these comments, especially as they are so ineffectual and not underscored by comprehension of the impact the reductions will likely have.

How OVA Works

OVA differs from traditional methods of value analysis as both the suppliers of overheads (those who incur the costs) and the customers of overheads (receivers of the services) are involved in determining the costs which should be cut. Ultimately it is Senior Management who will decide where costs will be cut, guided by the views of both supplier and customer.

OVA How To

There are six steps you’ll need to follow to execute an overhead value analysis:

- Step 1: Define the ideal service and output.

- Step 2: List all of the activities currently performed and their costs.

- Step 3: The customer evaluates the service and it’s output. Customers are asked to evaluate both the quality of the current output and also suggest any improvements which they think should be made.

- Step 4: Identify the necessary cost savings. This step forces those involved to make a statement about the relative priorities of the services provided and their output.

- Step 5: Decide whether activities should be eliminated, changed in some way, automated, integrated or outsourced.

- Step 6: Implement the savings which have been identified in the previous five steps.

This may sound convoluted and complex, but overhead value analysis can be implemented quickly if necessary. However, the process will typically not be painless as usually 70% plus of overhead costs are people related with most savings coming from headcount reductions. Because of this, if you are a program manager being asked to lead such a change, it is important to engage people throughout the overhead value analysis process, understand how to lead change, and also how to communicate based on where people are on the emotional change curve.